When a car lease is about to end, it’s easy to assume that the script is already written. You’re going to return the vehicle, pay whatever final charges show up, and start shopping again. But that is not always the smartest move. In fact, the last time I was in that situation, I realized I could sell my leased car for more flexibility and more value than I initially expected.

Car costs are still stubbornly high. In Q4 2025, the average monthly payment on a new-vehicle loan reached $767, while the average used-car listing price hit $26,043 in December 2025. When replacing a car is this expensive, the last thing you want to do is make a rushed lease-end decision just because you think you only have one path forward.

Slow down and look at the numbers

When the term ends, you can generally return the vehicle and pay any applicable end-of-lease fees, but there are other options, and it comes down to timing, flexibility, and personal finance.

Let’s explore what’s possible.

Option 1: Return the car and walk away

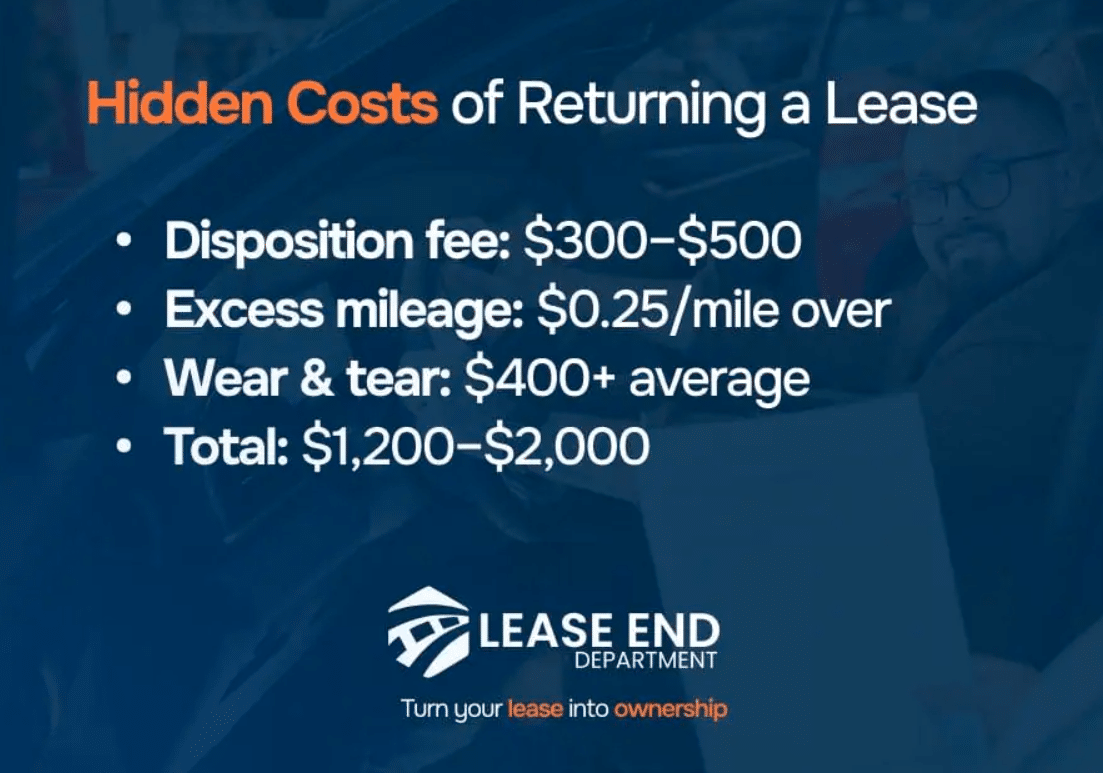

Sometimes the obvious option is the right one. If the car no longer fits your life, returning it may be the cleanest exit. But if you are over your mileage allowance or face a disposition fee, the final bill may be larger than expected. That is why the smartest version of a return is a prepared return.

Review the contract, estimate your mileage exposure, fix any obvious cosmetic issues if they are worth fixing, and understand what the lender considers normal wear versus billable damage. Excess mileage and wear-and-tear fees are common lease-end issues.

[Source: Lease End Department]

Returning the car usually makes the most sense when the vehicle’s market value is not especially favorable relative to the buyout price, or when you want maximum simplicity and minimum hassle.

Option 2: Buy the car if the math works in your favor

Your lease agreement usually includes a purchase option, often called the residual value or buyout price. That number was set earlier, before the lease began. If the car has held its value better than expected, buying it at lease end can be a smart move.

There is also the practical advantage of knowing the car’s history. You know how it was driven and how it was maintained, and there’s a lot of value in that.

This option can be especially attractive when replacement costs are high. With new-vehicle payments and used-car prices still elevated, keeping a car you already know can be a more rational move than jumping into a more expensive replacement.

Still, this is not an automatic yes. The buyout only makes sense if the total cost works. You need to compare the purchase price, taxes, registration, financing cost if you need a loan, and expected maintenance over the next few years.

Option 3: Sell or trade the car if there is equity in it

The basic math here is basically the same as in the previous option. If your car’s market value is higher than the buyout amount plus any related fees, there may be value to unlock.

Depending on your lender’s rules and your contract, the exact process varies, and some leasing companies place restrictions on who can buy the vehicle, so the first step is always to ask for your payoff quote and confirm your options directly with the lessor.

Option 4: Extend the lease for breathing room

Not everyone is ready to decide immediately, and sometimes that is okay.

If you need a little time to line up your next move, some lenders may allow a short lease extension, but it is generally a short-term solution and may be limited to as much as six months, if approved at all.

This can be useful if you are waiting on a new car delivery or expecting a life change, for example.

Asking the right questions

All too often, people worry about what sounds normal or even what the dealership expects. They do not stop to ask whether their transportation needs have changed or whether cash flow feels tighter than it used to.

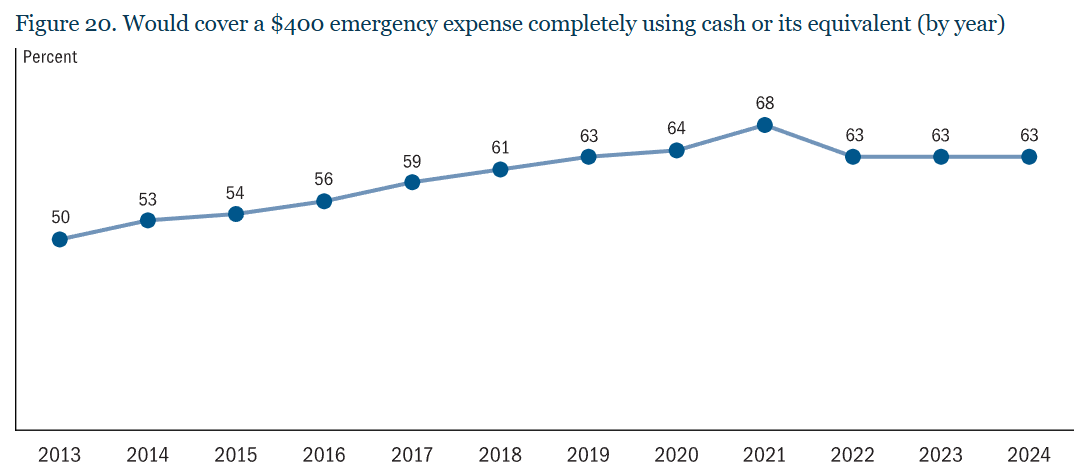

In 2024, only 63% of adults said they could cover a $400 emergency expense with cash or its equivalent, and just 55% said they had savings set aside for three months of expenses. So, even a “normal” car decision can put pressure on a household budget if it is made too casually.

[Source: Federal Reserve]

How to decide

Work through the options in this order:

- Find the buyout amount, mileage allowance, and any likely end-of-lease fees.

- Then check what similar cars are selling for and what dealers or car-buying platforms would actually offer you today.

- After that, estimate your next-step cost in each scenario: return it, buy it, sell it, or extend it.

- Finally, bring preferences into the picture. If buying the car saves money but you hate driving it, that matters. Also, if you are already mentally overloaded, the best option for your mental health may be worth more than the financially optimal one.

When each option tends to make sense

- Returning the car usually makes sense when you are over miles, or the buyout math is weak.

- Buying it tends to make sense when the residual value is attractive, and the car has been reliable.

- Selling or trading it can make sense when the market value is meaningfully above the payoff figure and your contract allows a path to capture that value.

- Extending the lease makes sense when you need a little breathing room and have a specific reason for waiting.

None of these options is universally best, but they all exist, and it’s up to you to choose which one is best for your situation. The best move depends less on what is standard and more on what the numbers, the contract, and your life say right now.

So, treat the end of your lease like an opportunity to compare outcomes, rather than just completing paperwork.

{kind=link}