Coinbase does report certain user activity to the IRS, and many crypto investors are surprised by how much information can actually be shared.

If you sell crypto, trade coins, earn staking rewards, or receive crypto income through Coinbase, your activity may be reported through IRS tax forms and account records.

Crypto taxes have become a major focus for the IRS, and Coinbase now follows stricter reporting rules than ever before.

This blog explains what Coinbase reports, which transactions are taxable, what forms you may receive, and what happens if you forget to report crypto taxes.

What Coinbase Reports to the IRS and Why It Matters

Coinbase reporting to the IRS means the exchange sends your tax information directly to the federal government. The IRS cross-checks that data against your tax return.

If what you filed does not match what Coinbase reported, you may get a notice, a penalty, or an audit. The IRS treats cryptocurrency as property, not currency.

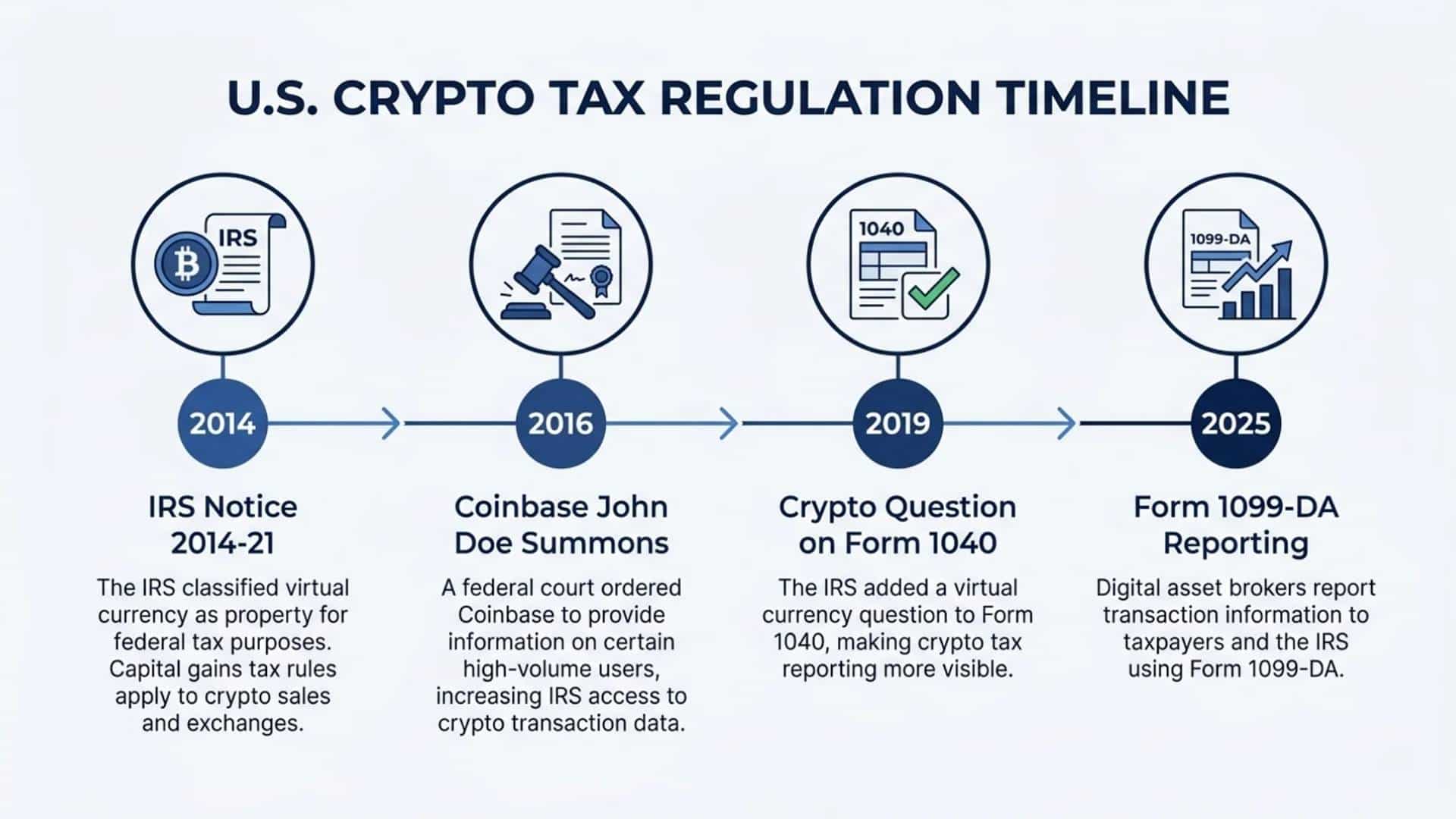

That rule comes from IRS Notice 2014-21, which has been the law since 2014. Every time you sell crypto, trade one coin for another, or earn crypto as income, that is a taxable event.

Coinbase acts as a reporting broker. Like a brokerage firm that reports your stock sales, Coinbase is legally required to report certain transactions to the IRS on your behalf.

Coinbase Tax Forms Explained

Coinbase currently uses two forms to report your activity to the IRS. Knowing which one applies to you is the first step to filing correctly.

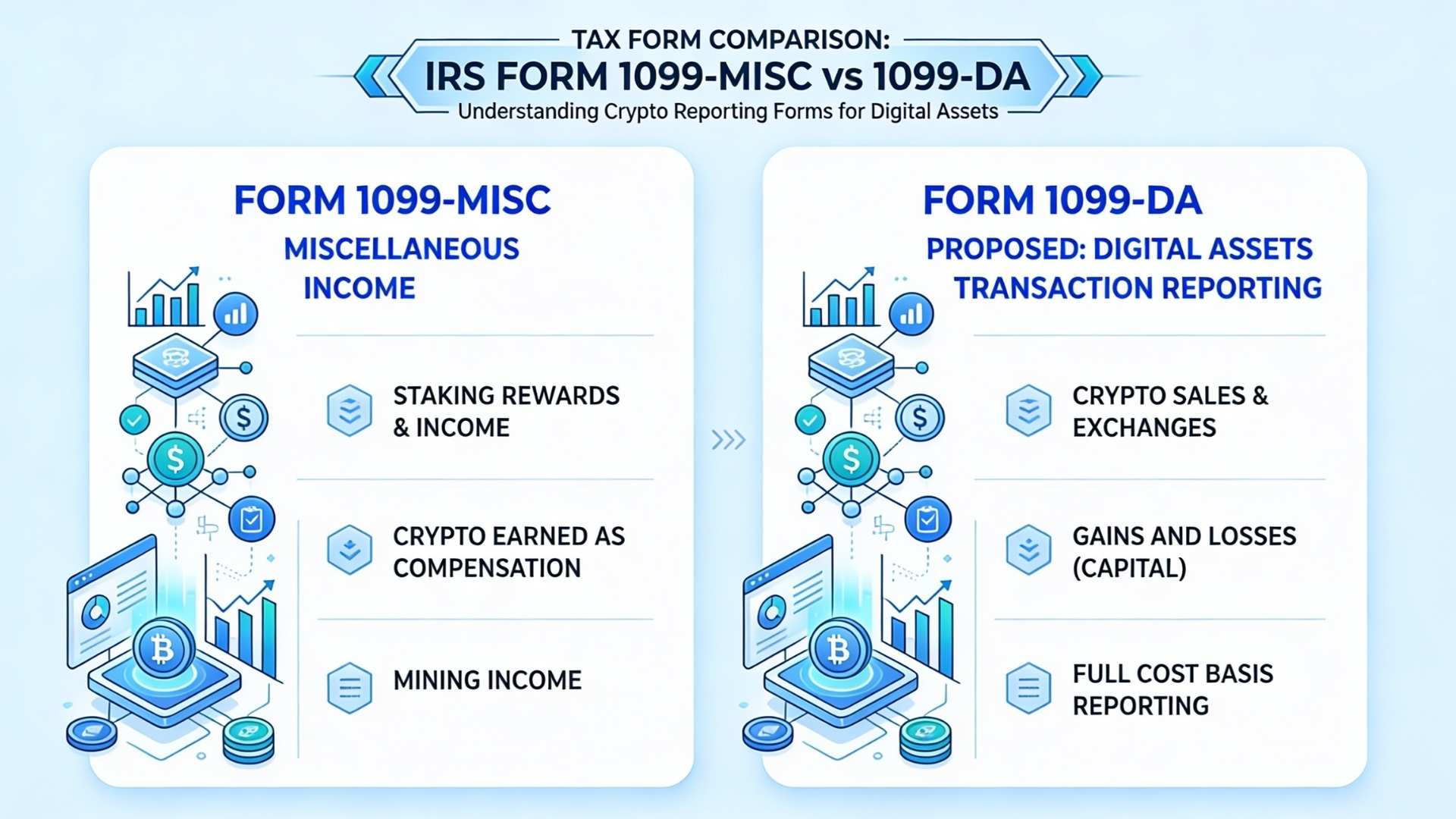

1. Form 1099-MISC: Coinbase sends Form 1099-MISC to users who earned $600 or more in crypto.

- Staking rewards

- Referral bonuses

- Learning rewards (Coinbase Earn)

- Other miscellaneous crypto income

Both you and the IRS get a copy of this form. If you received a 1099-MISC from Coinbase, that income must appear on your federal tax return, no exceptions.

2. Form 1099-DA: This is the big change. The IRS created Form 1099-DA specifically for digital asset brokers.

Under the Infrastructure Investment and Jobs Act, Coinbase and other crypto exchanges must file this form starting with the 2025 tax year (to be reported in early 2026).

Form 1099-DA will report:

- Proceeds from crypto sales

- Cost basis (what you originally paid)

- Gains and losses from exchanges

This form gives the IRS a much cleaner picture of your crypto activity than any previous form did.

Does Coinbase Report Every Transaction to the IRS?

No, not every single transaction triggers a direct IRS report. Right now, Coinbase primarily reports income events through Form 1099-MISC.

Starting with the 2025 tax year, Form 1099-DA will significantly expand reporting.

Here is what currently triggers a report:

| Activity | Reported to IRS? |

|---|---|

| Earning $600+ in staking or rewards | Yes (1099-MISC) |

| Selling crypto for cash | Starting 2025 (1099-DA) |

| Trading one crypto for another | Starting 2025 (1099-DA) |

| Buying crypto with USD and holding | No |

| Transferring between your own wallets | No |

The most important point: You must report all taxable crypto activity yourself, regardless of whether Coinbase sends you a form. The IRS does not excuse unreported gains because you did not receive a 1099.

IRS Has More of Your Coinbase Data Than You Think

The IRS has steadily expanded crypto enforcement over the past decade, and Coinbase data is now more visible to tax authorities than many investors realize.

From court orders to mandatory reporting forms, crypto transactions are no longer operating in a gray area.

In 2016, the IRS issued a legal summons, called a John Doe Summons, to Coinbase.

A federal court ordered Coinbase to hand over records for approximately 13,000 accounts that had transactions totaling more than $20,000 between 2013 and 2015.

The IRS used that data to send letters to users who had not reported crypto income. Some received CP2000 notices. Others were audited.

Beyond that, the IRS works with blockchain analytics companies, such as Chainalysis, to trace crypto transactions directly on public blockchains. Even if you move funds off Coinbase, the IRS has tools to follow the trail.

Starting in tax year 2019, the IRS added a crypto question to the top of Form 1040. Every US taxpayer must now answer whether they received, sold, or exchanged digital assets during the year.

Answering No when you did transact is a false statement on a federal tax return.

What if you did not receive a tax form from Coinbase?

Not getting a form does not mean you owe nothing. It just means your activity did not meet the current reporting threshold.

You are still legally required to calculate your gains and losses and report them. Here is how to get your transaction data:

- Log in toCoinbase. Go to Taxes in your account menu.

- Download your tax report. Coinbase generates a CSV of all transactions for the year.

- Use crypto tax software Tools like TurboTax Premium, TaxBit, CoinTracker, and Koinly, which connect directly to Coinbase via API and automatically calculate your gains and losses.

- Transfer totals to your 1040. Capital gains are reported on Form 8949 and Schedule D. Crypto income is reported on Schedule 1 or Schedule C.

How Short-Term and Long-Term Crypto Gains Are Taxed

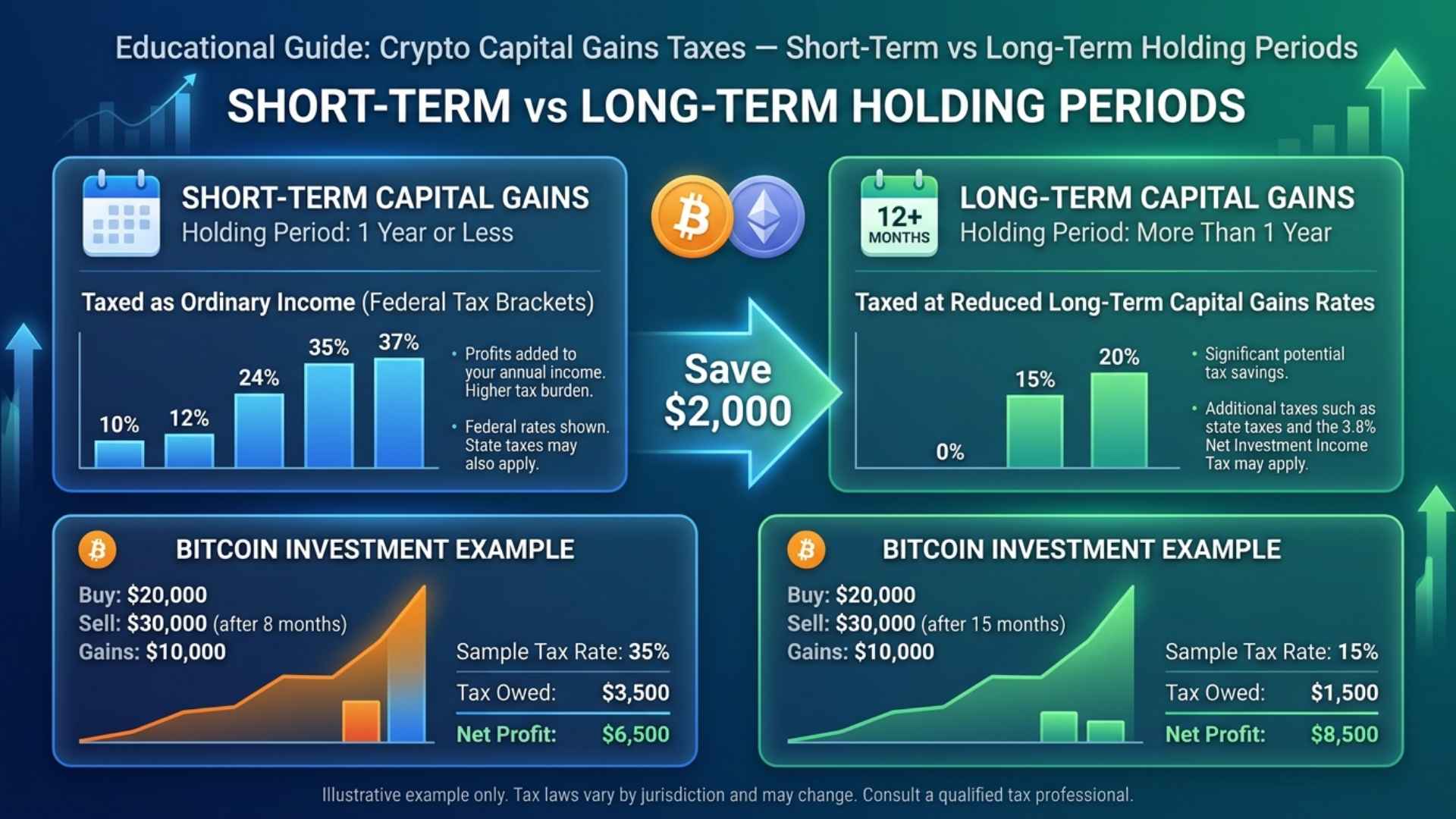

Your holding period directly changes how much tax you pay. This is one of the most important factors in crypto tax planning.

Short-term gains: Crypto held for less than one year before being sold is taxed as ordinary income at the same rate as your salary. Rates range from 10% to 37% depending on your total income.

Long-term gains: Crypto held for more than one year before selling is taxed at lower capital gains rates: 0%, 15%, or 20%, depending on income.

Common Mistake: Treating Crypto Trades as Non-Taxable

Many Coinbase users believe that swapping one crypto for another, say, Bitcoin for Ethereum, is not a taxable event. It is. The IRS treats every trade as a sale of the first asset. You owe tax on any gain at the moment of the trade, even if you never touched US dollars.

What Happens If You Don’t Report Coinbase Income?

Unreported crypto income does not automatically mean you are in serious trouble with the IRS. Several correction options are available depending on your circumstances.

Option 1 – File an amended return: Use Form 1040-X to correct a past return. You can amend returns for up to 3 years from the original due date.

Option 2 – IRS Voluntary Disclosure Program (VDP): For more serious cases, multiple years of unreported income or large amounts, the IRS Voluntary Disclosure Program allows you to come forward on your own terms.

Coming forward voluntarily puts you in a far better position than waiting for the IRS to send a notice.

Penalties for non-reporting can include:

- Back taxes owed plus interest

- A 20% accuracy-related penalty

- A 25% failure-to-file penalty

- In cases of willful fraud, criminal penalties (rare for simple omissions)

Talking to a CPA or tax attorney who knows crypto is strongly recommended if you have multiple years of unreported activity.

How to Report Coinbase Transactions

Here is a clean process for filing your Coinbase activity correctly:

Step 1: Collect your Coinbase transaction history. Download your full transaction CSV from the Coinbase Taxes section. Do this for every tax year you need to file.

Step 2: Identify your taxable events. Taxable events include: selling crypto, trading crypto for crypto, spending crypto on goods, and earning staking or reward income.

Non-taxable events include buying crypto with cash, holding it, and transferring it between your own wallets.

Step 3: Calculate gains and losses. For each sale or trade: Gain or Loss = Sale Price minus Cost Basis. Cost basis is what you originally paid, including any fees.

Step 4: Separate short-term and long-term gains. Group transactions by holding period. Short-term (under one year) and long-term (over one year) are reported separately.

Step 5: Complete Form 8949. List each taxable transaction on Form 8949. Total the gains and losses.

Step 6: Carry totals to Schedule D. Schedule D summarizes your net capital gain or loss and feeds into your Form 1040.

Step 7: Report earned income separately. Staking rewards and referral income are ordinary income. Report these on Schedule 1, Line 8z, or Schedule C if you are running a crypto-related business.

Coinbase vs Other Crypto Exchanges

Coinbase is a US-based, federally regulated exchange. That means it must comply with IRS reporting rules just like a stock brokerage.

Other exchanges have different situations:

| Exchange | Based in | US IRS Reporting |

|---|---|---|

| Coinbase | USA | Yes, forms sent to the IRS |

| Kraken | USA | Yes, required to comply |

| Binance.US | USA | Yes, a US-regulated entity |

| Offshore DEXs | Varies | Not directly, but blockchain is public |

Using a decentralized exchange (DEX) or a foreign exchange does not make your gains invisible to the IRS. The IRS can trace on-chain activity using blockchain analytics tools.

Your legal obligation to report does not depend on whether you received a 1099.

Conclusion

Coinbase does report to the IRS, and those reporting requirements are expanding, not shrinking. The rollout of Form 1099-DA in 2025 means the IRS will soon automatically have a detailed record of your sales and trades.

The steps forward are simple. Download your Coinbase tax reports, calculate your gains and losses, and file accurately.

If you missed prior years, file an amended return now before the IRS reaches out. A proactive correction costs far less than penalties do.

If your situation is complex, with a large portfolio, multiple exchanges, or missed years, a tax professional who knows digital assets can help you sort it out cleanly.

Have questions about your filing? Drop them in the comments below.

Frequently Asked Questions

Does the IRS Know if I Have Crypto?

Yes, through mandatory exchange reporting, blockchain analytics, and dedicated enforcement operations, the IRS has built a sophisticated system to track digital assets and match on-chain activity directly to your identity.

Why am I Limited to $3000 on Coinbase?

Your $3,000 Coinbase limit acts as an automated risk-management threshold. Coinbase dynamically determines purchase and deposit limits based on your account age, transaction history, region, and verification level.

Can I cash out $100,000 from Coinbase?

Yes, you can cash out $100,000 from Coinbase, assuming your account is fully verified (KYC completed) and your funds are held in a supported fiat currency or stablecoin.